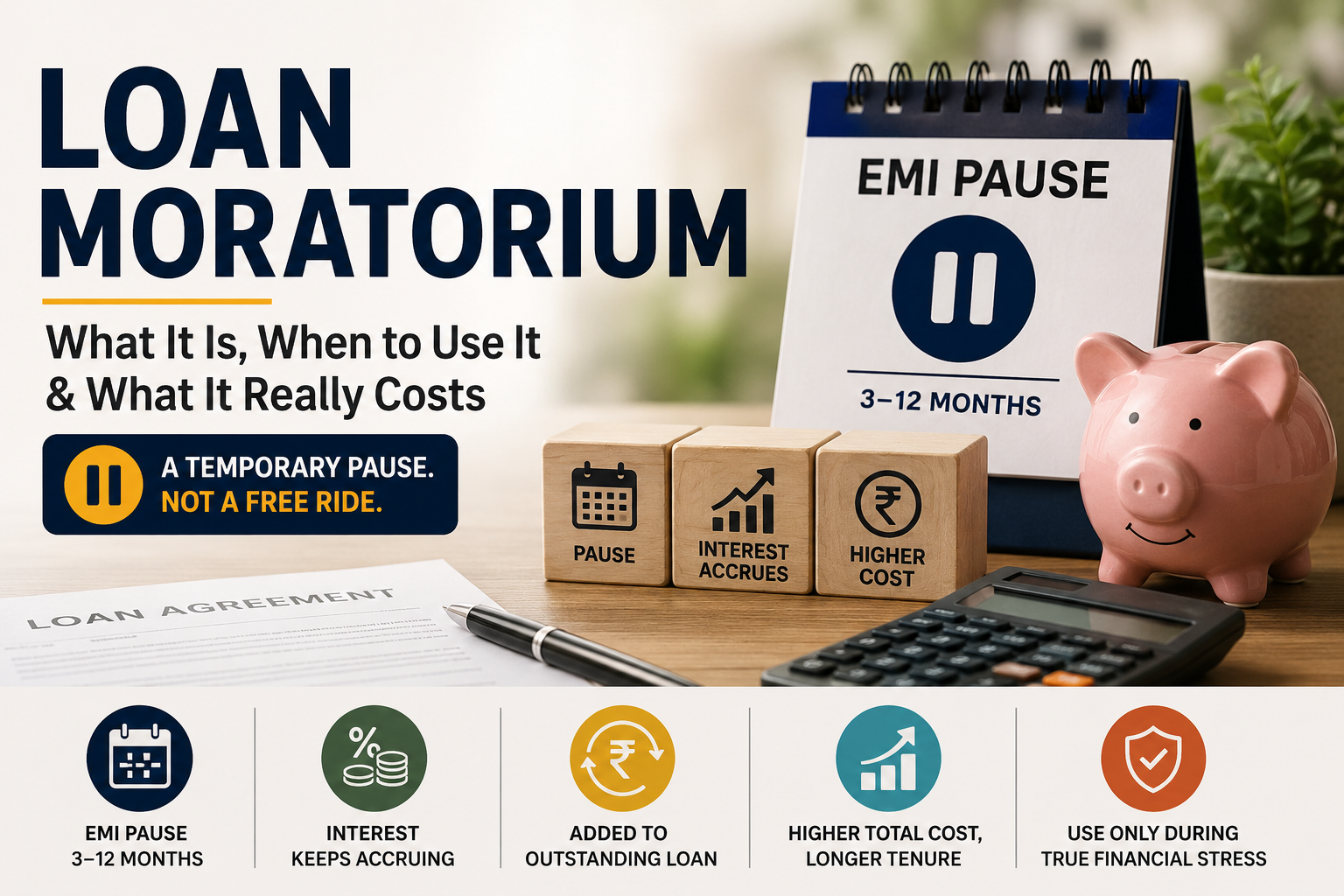

What Is Loan Moratorium and When Should You Use It?

A loan moratorium is a temporary period during which a borrower is allowed to pause or defer EMI payments without being marked as a defaulter. In this guide, you’ll learn what a moratorium really means, how the deferred interest works, and when you should use it.

Quick Summary

- A moratorium is an EMI pause, typically granted for 3–12 months, allowed by lenders during financial hardship or under-construction periods.

- Interest continues to accrue during the moratorium and is added to the outstanding principal — it’s deferred, not waived.

- Common scenarios: under-construction property, RBI-mandated relief, education loan study period, job loss.

- Using a moratorium increases your total loan cost — sometimes by lakhs over the original tenure.

- It’s a short-term liquidity tool, not a way to reduce loan cost.

What Is Loan Moratorium?

What does it mean?

A loan moratorium is a lender-approved pause on your EMI payments for a defined period. The borrower is not classified as a defaulter, and there is no negative impact on the CIBIL score. However, interest continues to accrue and is added to the principal, increasing total dues.

How does it work?

When a moratorium is granted, the lender stops collecting EMIs. Interest still accrues every month and is capitalised — added to the principal. After the moratorium ends, the bank recalculates your loan by extending the tenure (most common), increasing the EMI, or asking for a lump-sum payment.

Types of Moratoriums

| Type | Who Grants It | Typical Duration |

|---|---|---|

| Construction moratorium | Lender (built into loan) | Until possession (1–3 years) |

| Hardship moratorium | Lender (case-by-case) | 3–6 months |

| Policy moratorium | RBI directive | 3–6 months (rare) |

| Education loan moratorium | Lender (built into loan) | Course duration + 6–12 months |

When to Use (and When Not to Use) a Moratorium

Opt for a moratorium only if: You face genuine short-term liquidity stress — job loss, major medical emergency — and have no other source to cover EMIs.

Avoid a moratorium if: You have alternative liquidity, or if your stress is short-term enough to manage by reducing other expenses.

Practical Tips

- Calculate the additional interest cost before opting in.

- Use moratorium funds wisely — don’t spend the EMI savings on lifestyle.

- Resume EMIs as soon as possible.

- Consider partial EMIs (interest-only) instead of full pause if your lender allows it.

Common Mistakes to Avoid

- Treating a moratorium as a “free EMI holiday” — interest accrues every single month.

- Opting in just because it’s offered when you can comfortably continue paying.

- Not getting the revised loan schedule in writing.

FAQ

Does a loan moratorium hurt my CIBIL score?

A formally approved moratorium does not directly hurt your CIBIL score — missed EMIs during the moratorium are not reported as defaults.

How is interest calculated during a moratorium?

Interest accrues on the outstanding principal at your existing loan rate every month and is capitalised at the end.

Can I take a partial moratorium?

Some lenders allow paying just the interest portion of the EMI during the pause, which reduces the compounding effect significantly.

Is a moratorium the same as loan deferment?

Loan deferment is a broader term. A moratorium specifically pauses EMI payments for a defined period.

What was the COVID-19 loan moratorium?

In March 2020, RBI permitted banks to offer a 6-month moratorium on EMI payments due to the pandemic’s economic impact.