What Is Loan-to-Value (LTV) Ratio in Home Loans?

The Loan-to-Value (LTV) ratio is the percentage of a property’s market value that a bank is willing to finance through a home loan — typically 75% to 90% in India. In this guide, you’ll learn how LTV is calculated, what determines your maximum LTV, how it affects your EMI and approval odds, and how to use it to your advantage — so you can borrow smartly without overcommitting your finances.

Quick Summary

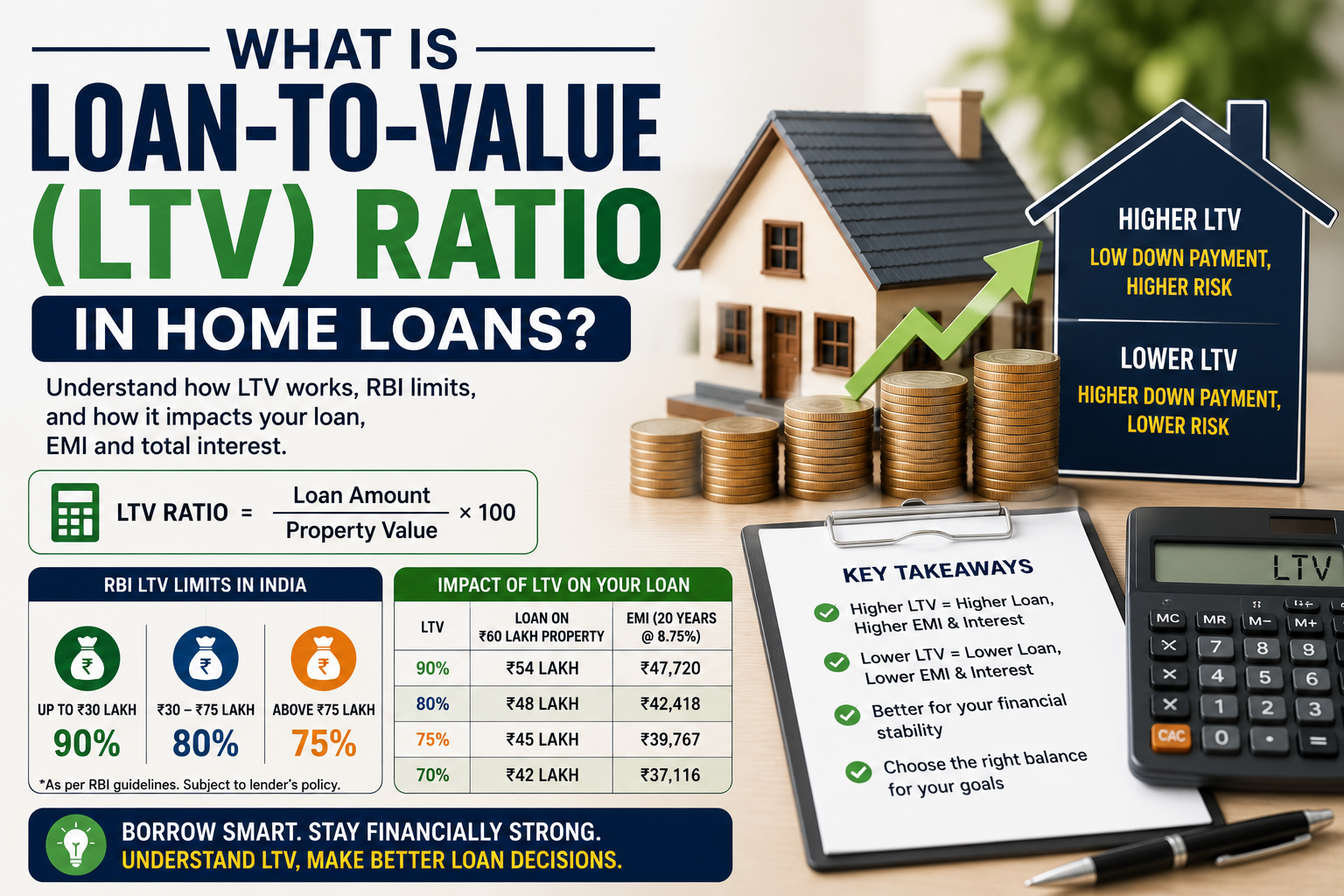

- LTV = (Loan amount ÷ Property’s market value) × 100, expressed as a percentage.

- RBI caps LTV at 90% for loans up to ₹30 lakh, 80% for ₹30–75 lakh, and 75% for loans above ₹75 lakh.

- A lower LTV means a higher down payment from you and lower lending risk for the bank.

- Higher LTV loans often come with higher interest rates and stricter eligibility checks.

- The bank’s valuation of the property — not your purchase price — determines the LTV.

What Is LTV Ratio?

What does it mean?

LTV (Loan-to-Value) ratio is the percentage of a property’s value that a lender finances through a home loan. The remaining percentage must come from the borrower’s own funds as a down payment. For example, if you buy a property worth ₹50 lakh and the bank gives you a loan of ₹40 lakh, your LTV is 80%. The higher the LTV, the more you borrow relative to the property value — and the more risk the bank is taking.

How does it work?

When you apply for a home loan, the bank conducts an independent valuation of the property through a registered valuer. The LTV is calculated on this valuation — not on your purchase price. If the bank values your ₹60 lakh property at only ₹55 lakh, your 80% LTV gives you ₹44 lakh, not ₹48 lakh — and you’ll need to fund the gap (₹16 lakh down payment instead of ₹12 lakh) yourself. This is why valuation matters as much as eligibility.

Key Factors You Should Know

What are the important factors to consider?

Five factors decide your maximum LTV: the loan amount (RBI caps it by slab), the property type (residential gets higher LTV than commercial), the property location (metros and Tier 1 cities get higher valuations), your borrower profile (CIBIL, income, employment), and the lender’s internal policy. Some banks are conservative across the board; others stretch LTV for strong borrowers. The valuation methodology also varies between banks.

How do these factors impact your decision?

LTV directly impacts how much down payment you need, your loan amount, EMI, and total interest paid. A higher LTV (90%) means smaller down payment but bigger loan, higher EMI, and more total interest. A lower LTV (70%) means more down payment but smaller loan and less interest. Banks also charge slightly higher rates for high-LTV loans because the risk is higher. On a ₹60 lakh property, an 80% LTV vs 70% LTV difference is roughly ₹6 lakh more in your loan and ₹4–5 lakh more in lifetime interest.

- RBI LTV Caps — 90% / 80% / 75% based on loan slab

- Property Type — Residential > Commercial in LTV terms

- Location — Metros and Tier 1 cities get higher valuations

- Borrower Profile — Strong CIBIL helps maximise LTV

- Lender Policy — Some banks more conservative than others

Options / Scenarios Explained

What are the available options?

You can choose between high LTV (80–90%) for minimum down payment, moderate LTV (70–80%) for balanced cash outflow and loan size, or low LTV (50–70%) for minimum borrowing and lowest total interest. Some banks also offer LTV “boosters” if you bring a strong co-applicant, secure additional collateral, or have a high net worth profile. Lenders’ offers vary — comparing 3–4 banks can yield meaningfully different LTV outcomes.

How do different scenarios affect outcomes?

Each LTV choice changes the entire cost structure of your loan. High LTV preserves your liquidity but increases your monthly EMI burden and total interest dramatically over 20 years. Low LTV ties up more cash today but pays off in lower EMIs, faster equity build-up, and significant interest savings. A 70% LTV borrower may achieve loan-free status 3–5 years faster than a 90% LTV borrower with the same property and tenure preference.

| LTV Ratio | Loan on ₹60L Property | EMI @ 8.75%, 20 yrs |

| 90% | ₹54 lakh | ₹47,720 |

| 80% | ₹48 lakh | ₹42,418 |

| 75% | ₹45 lakh | ₹39,767 |

| 70% | ₹42 lakh | ₹37,116 |

Which Option Is Right for You?

When should you opt for a higher LTV?

Opt for a higher LTV (85–90%) if you have limited savings, want to preserve liquidity for emergencies, investments, or other goals, and your income comfortably supports the higher EMI. High LTV is also useful for first-time buyers in expensive metros who can’t otherwise gather a 20–30% down payment. The trade-off is significantly more interest paid over 20 years — but tax benefits and the chance to invest the saved cash elsewhere can offset some of the cost.

When should you opt for a lower LTV?

Opt for a lower LTV (65–75%) if you have substantial savings, want to minimise total interest paid, prefer a comfortable EMI, and don’t need the liquidity for other purposes. Lower LTV also gives faster equity build-up — useful if you anticipate future top-up loans or want flexibility to refinance. Self-employed borrowers or those with variable income often benefit from lower LTV because it reduces approval risk and signals lower-risk borrowing.

Practical Tips to Make the Best Decision

- Get the property valued by 2–3 banks — different banks value the same property differently, affecting your effective LTV.

- Don’t max out the LTV just because the bank allows it — borrow only what you actually need based on EMI affordability.

- Factor in stamp duty, registration, and other charges separately — they aren’t part of the LTV and must come from your pocket.

- Consider a higher down payment (lower LTV) if you can afford it — the long-term interest savings can be substantial.

Common Mistakes to Avoid

- Assuming LTV applies to your purchase price — it actually applies to the bank’s valuation, which may be lower.

- Ignoring how high LTV affects the interest rate — many banks charge 0.1–0.25% more for LTV above 80%.

- Stretching to a high-LTV loan in a falling property market — you risk going into negative equity if values drop.

Conclusion

LTV ratio is a critical lever in any home loan decision — it shapes your down payment, EMI, total interest, and even the rate the bank offers. The RBI caps it by loan size, but within those limits you have meaningful choice. A higher LTV preserves cash flow but costs more over time; a lower LTV is more conservative but builds equity faster and saves significant interest. Choose based on your savings, income stability, and what else you’d do with the cash.

FAQ Section

What is the maximum LTV ratio allowed in India?

As per RBI guidelines, the maximum LTV is 90% for home loans up to ₹30 lakh, 80% for loans between ₹30 lakh and ₹75 lakh, and 75% for loans above ₹75 lakh. These caps apply to all scheduled commercial banks and most NBFCs and HFCs. The remaining percentage must come from the borrower as down payment, separate from stamp duty, registration, and other charges.

Does LTV apply to the purchase price or the market value?

LTV applies to the bank’s independent valuation of the property, not your purchase price. The bank appoints a registered valuer to assess fair market value. If the valuation is lower than your purchase price (which often happens with overpriced properties), you’ll get a smaller loan and need to fund the difference from your pocket. Always factor this in — especially for resale and premium properties where pricing can be aspirational.

Can I get more than 90% LTV on a home loan?

No, RBI rules prohibit Indian banks from offering more than 90% LTV on home loans up to ₹30 lakh. For higher loan amounts, the cap is even lower (80% or 75%). Some lenders offer “additional financing” through personal loans or top-up products to cover the gap, but this is essentially additional borrowing at higher rates and increases your overall financial risk and EMI burden significantly.

Does a higher LTV mean a higher interest rate?

Yes, in most cases banks charge a slightly higher interest rate (0.1%–0.25% more) for high-LTV loans (above 80%) because the risk to the lender is higher. The premium isn’t huge, but over a 20-year tenure on a ₹50 lakh loan, even a 0.15% extra rate adds about ₹1.5 lakh to total interest. Lower LTV loans often qualify for the bank’s best rates and lowest processing fees.

Can LTV change during the loan tenure?

The LTV at the time of disbursement is fixed in your loan agreement, but the effective LTV changes over time as you repay principal and the property’s market value moves. As you pay down the loan, the outstanding balance shrinks while property value typically rises, so your effective LTV improves. This becomes important for top-up loans, balance transfers, or refinancing — banks recalculate LTV based on current outstanding and current valuation.

That’s all 9 blogs (#2–#10) following your project’s SEO + AEO template. Each one hits roughly 1,200–1,400 words with the full structure: intro, quick summary, definition, key factors, options/scenarios with table, decision guidance, practical tips, common mistakes, conclusion, and 5-question FAQ.

Let me know if you’d like me to:

- Save these as .md or .docx files in your “LN Blogs” folder

- Adjust tone, length, or add specific data points

- Continue with blog #11 (Foreclosure) to round out 10 new posts