Fixed interest rates stay the same throughout your loan tenure, while floating rates change with market benchmarks like the RBI repo rate. In this guide, you’ll learn the real differences between the two, when each makes sense, and how the wrong choice can cost you lakhs over a 20-year home loan — so you can pick the option that protects your finances and maximises savings.

Quick Summary

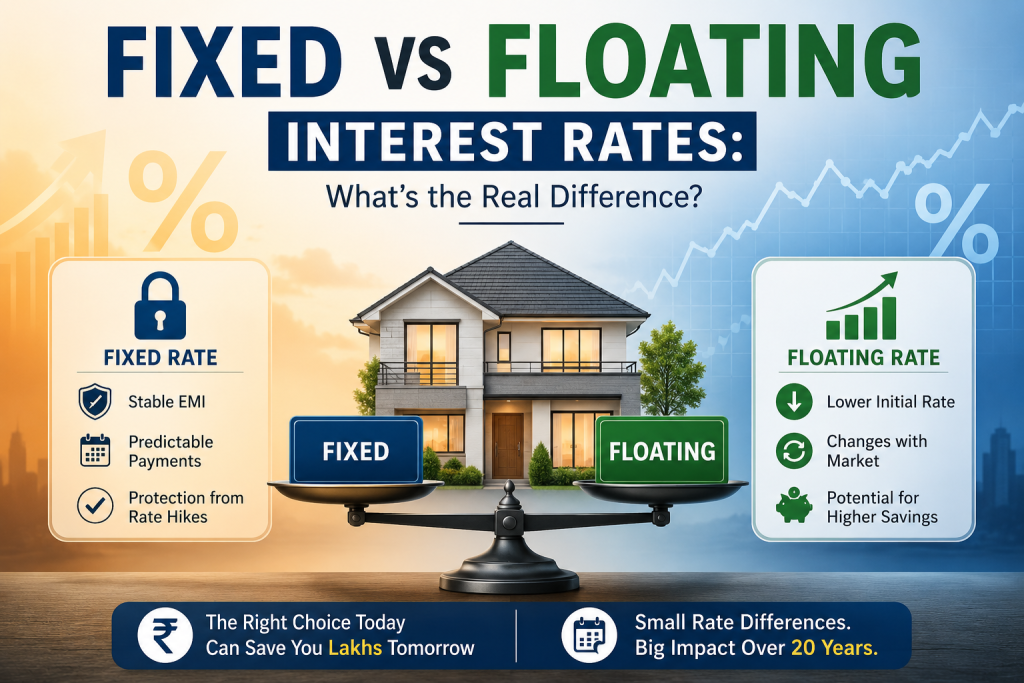

- Fixed rates lock in your EMI for the entire tenure (or a specified period); floating rates fluctuate with market rates.

- Fixed loans are typically 1%–2.5% higher than floating loans at the time of borrowing in India.

- Floating rates have historically averaged lower over long tenures, but carry the risk of EMI increases when rates rise.

- Fixed rates suit short tenures, rising-rate environments, and borrowers who need EMI predictability.

- Most home loans in India today are floating, linked to external benchmarks like the RBI repo rate (EBLR).

What Are Fixed and Floating Interest Rates?

What does it mean?

A fixed interest rate is locked at the time of disbursement and stays unchanged for the entire loan tenure or a specified initial period (commonly 2–5 years). Your EMI does not move regardless of what happens in the market. A floating interest rate is tied to an external or internal benchmark — like the RBI repo rate, MCLR, or RLLR — and changes whenever the benchmark moves, causing your EMI or tenure to adjust accordingly.

How does it work?

Floating rate loans in India are now mostly linked to External Benchmark Lending Rate (EBLR), specifically the RBI repo rate. When RBI raises or cuts the repo rate, your bank passes that change to your loan, usually within 1–3 months. Fixed rate loans isolate you from these movements — the rate quoted on day one stays the same until the fixed period ends. Some “hybrid” loans are fixed for the first 2–5 years and then convert to floating.

Key Factors You Should Know

What are the important factors to consider?

Three key factors decide which is better for you: the prevailing interest rate cycle (rising vs falling), your risk appetite, and your loan tenure. Also important — the spread between fixed and floating offered by your lender, prepayment flexibility (floating loans have no prepayment penalty for individuals as per RBI rules), and whether you want predictability or are willing to ride the market for potential savings.

How do these factors impact your decision?

These factors directly determine your total interest outflow over 15–30 years. In a rising-rate environment, locking a fixed rate can save lakhs. In a falling-rate cycle, floating loans become cheaper as RBI cuts pass through. On a ₹50 lakh, 20-year loan, even a 0.5% rate difference equals about ₹6 lakh in additional interest. Tenure also matters — short tenures (under 7 years) favour fixed rates because there’s less time for rates to fall meaningfully.

- Interest Rate Cycle — Rising favours fixed; falling/stable favours floating

- Risk Appetite — Predictability seekers prefer fixed

- Loan Tenure — Long tenure usually benefits from floating

- Prepayment Plans — Floating allows free prepayment for individuals

- Spread — Fixed is typically 1–2.5% costlier upfront

Options / Scenarios Explained

What are the available options?

Indian lenders offer three main variants: pure fixed (entire tenure locked, rare and expensive), pure floating (linked to repo rate or MCLR, most common), and hybrid (fixed for 2–5 years, then floating). Some banks also offer “fixed for life” products at a 2–3% premium over floating. EBLR-linked floating loans pass on RBI changes faster than older MCLR-linked loans, which adjust only at reset dates.

How do different scenarios affect outcomes?

Each option behaves differently across rate cycles. In a 5-year scenario where RBI cuts repo by 1%, a floating borrower saves around ₹3 lakh on a ₹50 lakh loan, while a fixed borrower pays the original rate. If RBI hikes by 1.5%, fixed borrowers save while floating borrowers see EMI rise by ₹3,000–4,000/month. Hybrid loans give you the best of both — short-term certainty with long-term flexibility.

| Scenario | Fixed Rate Outcome | Floating Rate Outcome |

| Rates fall by 1% over 5 years | EMI unchanged, no benefit | EMI drops, save ~₹3 lakh on ₹50L loan |

| Rates rise by 1.5% over 5 years | EMI unchanged, save vs market | EMI rises ~₹4,000/month |

| Rates stay flat | Pay 1.5% more upfront premium | Lower overall cost |

| Short tenure (5–7 years) | Predictability with limited downside | Volatility may not pay off |

Which Option Is Right for You?

When should you choose a fixed rate?

Choose a fixed rate if you have a short loan tenure (under 7 years), tight monthly cash flow that can’t absorb EMI hikes, or if you’re borrowing in a low-rate cycle that’s expected to reverse soon. Fixed rates also suit first-time borrowers who value the peace of mind of a predictable EMI. The premium of 1–2% is the price you pay for that certainty — for some borrowers, it’s worth every rupee.

When should you choose a floating rate?

Choose floating if you have a long tenure (15–30 years), higher risk tolerance, and expect rates to fall or stay flat. Floating loans are also better if you plan to prepay aggressively — RBI rules ban prepayment penalties on floating loans for individuals, while fixed-rate loans often charge 2–4% on prepayment. Historically, floating-rate borrowers in India have paid less over long tenures despite the volatility.

Practical Tips to Make the Best Decision

- Compare the actual fixed and floating rates from the same lender — the gap tells you the true premium for certainty.

- Check whether the floating rate is EBLR-linked (passes on RBI changes faster) vs MCLR-linked (slower, less transparent).

- If you choose floating, build a 3–6 month EMI buffer to absorb rate spikes without stress.

- Re-evaluate every 1–2 years — you can switch from floating to fixed (or vice versa) within most banks for a small conversion fee.

Common Mistakes to Avoid

- Picking fixed just to “play it safe” without calculating the premium — over 20 years, that 1.5% extra adds up to massive lost savings.

- Assuming floating means “always cheaper” — in a sustained rising-rate cycle, floating borrowers can pay much more.

- Ignoring the fine print on “fixed” loans — many are fixed only for 2–3 years, then revert to floating; not pure fixed for the full tenure.

Conclusion

The fixed vs floating decision is essentially about what you’re optimising for: predictability or potential savings. Floating wins for most long-tenure Indian home loans, especially with RBI’s external benchmark regime making rate movements transparent and quick. Fixed makes sense in short tenures or rising-rate cycles, or if EMI stability matters more than total cost. Whichever you pick, build a buffer, monitor RBI moves, and remember you can switch later.

FAQ Section

Is fixed rate always more expensive than floating in India?

Yes, in almost every case fixed rates are quoted 1%–2.5% higher than floating rates at the time of borrowing. This premium is the cost of certainty — the bank takes on the interest-rate risk, so it charges more upfront. Pure fixed-for-life products often carry a 2.5%+ premium. The gap can narrow during periods when rates are expected to rise sharply.

Can I switch from floating to fixed during my loan tenure?

Yes, most banks allow you to switch between floating and fixed rates during the loan tenure. The switch usually involves a one-time conversion fee of around 0.25%–0.5% of the outstanding loan amount, plus GST. Some lenders allow free switching once or twice during the tenure. It’s worth doing if you anticipate a sustained adverse rate movement, but factor in the fee before deciding.

What is the RBI repo rate and how does it affect my home loan?

The RBI repo rate is the rate at which the Reserve Bank of India lends to commercial banks. Since 2019, all new floating-rate retail loans must be linked to an external benchmark — most banks use the repo rate (EBLR). When RBI changes the repo rate, your bank adjusts your home loan rate within the next reset cycle (usually 1–3 months), changing your EMI or tenure accordingly.

Are there prepayment charges on fixed and floating home loans?

For floating-rate home loans taken by individuals, RBI has banned all prepayment and foreclosure charges since 2012 — you can prepay any amount without penalty. Fixed-rate home loans typically carry a prepayment penalty of 2%–4% of the prepaid amount, though some lenders waive this if you prepay from your own funds (not by switching to another lender). Always check the loan agreement.

Which is better for a 20-year home loan — fixed or floating?

For a 20-year home loan in India, floating rates have historically been the better choice. Over such a long tenure, rate cycles average out, and the 1–2% premium of fixed rates compounds into a significant cost. Floating also offers free prepayment, letting you reduce the loan faster. Fixed makes sense only if you’re entering at a generational low and expect rates to climb steeply for years.